Ownership control, transnational corporations and financial power

Ownership control, transnational corporations and financial power

Power has always been an issue of particular importance for the social sciences, in general, and for Political Economy in particular. Many studies in this field, from different approaches, have wondered about the nature, structure and sources of power.

Particularly noteworthy are those authors –such us Susan Strange, Stephen Gill of Ulrich Beck– who have addressed a phenomenon of great importance to understand the reconfiguration of contemporary power relations: the expansion of private transnational actors.

The liberalization and transnational integration of capitals and markets have determined, according to these authors, a profound asymmetry between the enlargement of economic power on the one hand, and the underdevelopment, on the other hand, of political and regulatory frameworks that should control that power. These authors have realized a very interesting effort identifying, in this respect, the main characteristics of the power exerted by transnational private actors.

However, these studies and others like have been usually carried out by specialists from the field of Political Science, mainly by means of qualitative methodologies. More unusual are the works that analyze transnational corporations with empirical and quantitative methodologies.

In this regard, an outstanding study has been recently accomplished by Stefania Vitali, James B. Glattfelder and Stefano Battiston 1, specialists in Systems Design at the Swiss Federal Institute of Technology. “The Network of Global Corporate Control”, published by the prestigious PLoS ONE, has quickly gathered attention of other researchers and scientists, as well as the media worldwide, due to the significant progress achieved in mapping the transnational corporate power structure.

The research questions of the investigation are basically three: How is the world architecture of corporate ownership organized? How is control distributed in this network? Who are the key economic actors of the network?

It is well known that transnational corporations exert control over other subsidiaries, in many countries, through a web of direct and indirect shareholding relations. Nevertheless, the architecture of this network was not well known until now, nor the global distribution of the economic control or the identity of the major nodes. For example, are transnational corporations grouped together into clusters relatively isolated from each other, or do they form a densely connected network with a core/periphery structure? What kind of control do the main corporations exert over the rest? Despite the enormous importance this topic has for economic policy, research has been relatively limited to date.

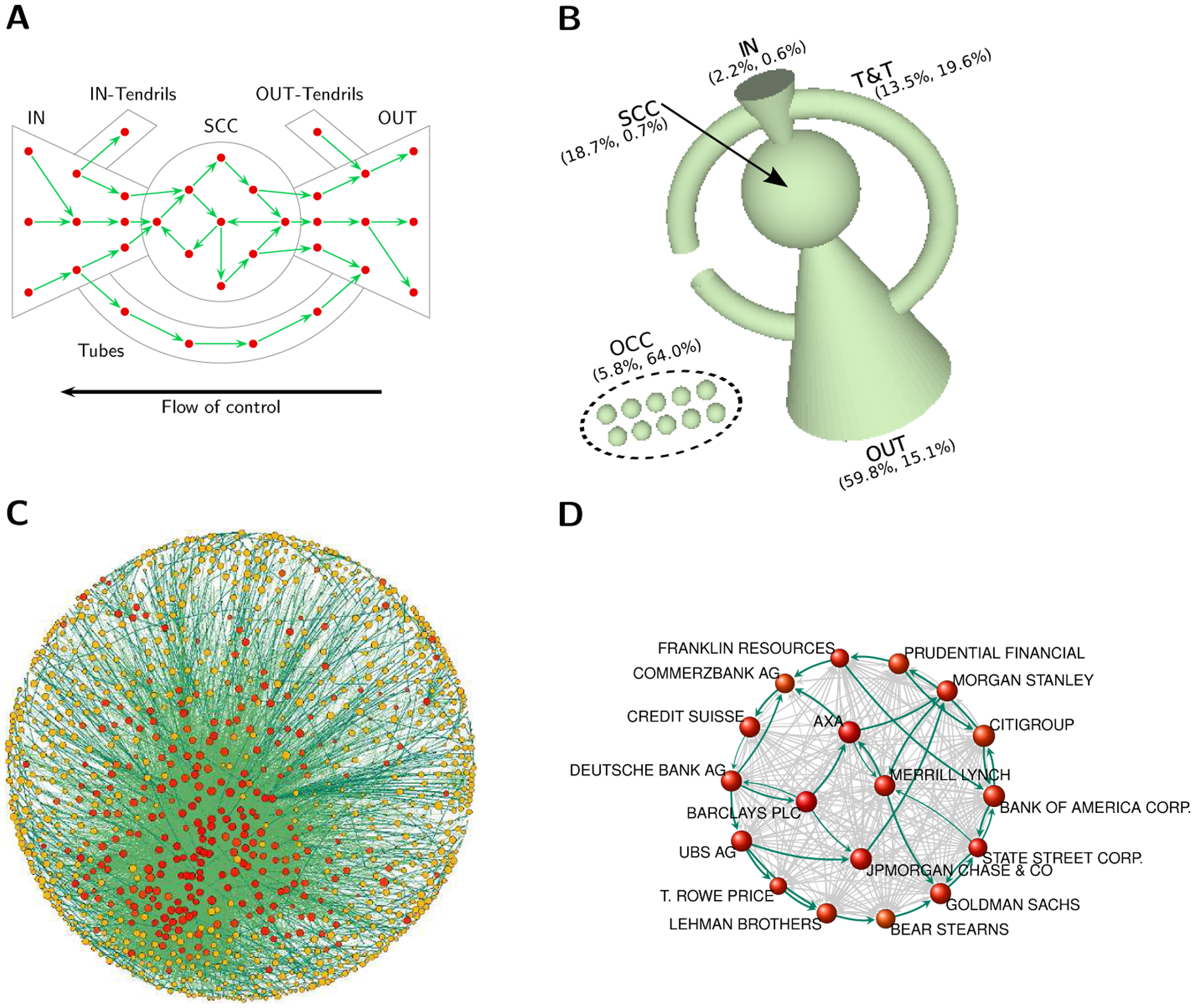

From Orbis database, produced by Bureau van Dijk (publisher of company information), and with 2007 data, Vitali, Glattfelder and Battiston analyze shareholding links of more than 43000 transnational corporations from 116 countries, defining a vast network of 600500 nodes and more than one million ownership ties.

Although other studies had previously developed similar economic analysis using methods from the field of complex networks –e.g., trade networks 2 or ownership networks 3 –, an empirical research of the structure of ownership control at a global level has never been realized before.

Two are the main results of “The Network of Global Corporate Control”. First, the authors map the topology of the network of corporate power. They find a network divided in many clusters of companies. However, the largest one, composed of 15491 firms, accounts for 94% of the total transnational corporations operating revenue. In the core of this cluster the authors find a small group of corporations (the so called Strongly Connected Component, a 0.7% of the total dataset, i.e. 295 companies, especially from Anglo-Saxon countries). Corporations from this core group (which accounts for 18.7% of the total operating revenue) are very strongly interconnected by mutual cross-shareholdings, resulting in a set of firms in which every member owns directly or indirectly shares from the rest of the members of the core group. As a result, 75% of the core’s share ownership remains in the hands of other companies of the kernel.

Secondly, the authors identify the global distribution of power in the network and the identity of major shareholders. Only 737 corporations accumulate 80% of the control of the transnational network. Control is proxied by the potential control over the corporations operating revenue. Thus, the authors find that network control is distributed much more unequally than wealth. In particular, the top corporations hold a control ten times larger than what could be expected based on their wealth.

These two important results are connected together, so that by combining the topological description of the network with control status the authors provide a complete characterization of the corporate power structure.

As expected, the most powerful transnational corporations tend to fit in the core of the network. Despite its small size, this core accumulates a high percentage of the total network control: a subset of 147 companies wields control, through an intricate web of shareholdings, over 40% of the operating revenue of all transnational corporations. In addition, this economic “super-entity” –as the authors name it– has almost full ownership control over itself. A particularly relevant aspect of this description of the top control-holders is that approximately 75% of them are financial institutions.

These outstanding results from Vitali, Glattfelder and Battiston deepen our understanding of transnational corporate power, completing the previous studies of Strange, Gill, Beck and other social scientists. But, these results also help economists to identify how the architecture of international financial power has led to the current economic crisis.

First, the strong economic and shareholding ties between financial corporations have sharpened systemic risks and the speed of contagion in times of crisis. Furthermore, the enormous concentration of power accumulated by these institutions has undermined the sovereignty of States and parliaments, encouraging a process of “regulatory capture” able to promote legislative changes beneficial to financial interests (removal of financial controls, deregulation of markets, increase of capital mobility). All this has led, as we know, to flawed risk management in financial institutions (and with them, in the whole economy), to the accumulation of toxic assets and to a development of financial activity not supported by real economic growth, determining the current crisis.

References

- Vitali, S., Glattfelder, JB. and Battiston, S. (2011) The Network of Global Corporate Control. PLoS ONE 6(10) DOI: 10.1371/journal.pone.0025995 ↩

- Fagiolo, G., Reyes, J. and Schiavo, S. (2009) World-trade web: Topological properties, dynamics, and evolution. Physical Review E, 79. http://arxiv.org/pdf/0807.4433.pdf ↩

- Glattfelder, JB. and Battiston, S. (2009) Backbone of complex networks of corporations: The flow of control. Physical Review E, 80. http://arxiv.org/pdf/0902.0878.pdf ↩

3 comments

[…] in Destacado, Hablando de economía, Profesores No comments Nacho Álvarez Peralta Published in Mapping Ignorance Research Associate at the Complutense Institute of International Studies (ICEI) Assistant Professor […]

[…] Publicado en Mapping Ignorance […]

[…] Network of Global Corporate Control clearly shows the primary agents who benefit from this bounty of invisible tax on our savings […]