Experimenting with markets

Experimenting with markets

Markets are the most studied economic mechanism for two main reasons. First, they have existed in most societies. Second, at least since Adam Smith we have learned some of the interesting properties they possess.

In particular, the modern General Equilibrium Theory, in its standard version, asserts that rational agents interacting in a competitive market with no externalities (e.g., pollution), no public goods (e.g., a central park), and no informational problems will trade at the competitive equilibrium and produce efficient allocations of resources and commodities. One of the objections to this model is that the conditions are rarely met in real life.

One must understand, however, that these conditions are sufficient, and by no means necessary. Further, even if some of them are not satisfied and the market fails to achieve efficiency, one must still consider whether another economic mechanism exists that can outperform the market in this respect. In this article, I will restrict the discussion to the predictive power of the equilibrium theory (from which the efficiency property follows). To this goal I am going to show some of the theoretical and experimental evidence that favors the hypothesis of competitive markets reaching the theoretical equilibrium. Other considerations, like the study of equality, or the study of other empirical or historical evidence are not discussed here. Also, the markets we are dealing with do not include financial derivatives markets (like futures and securities).

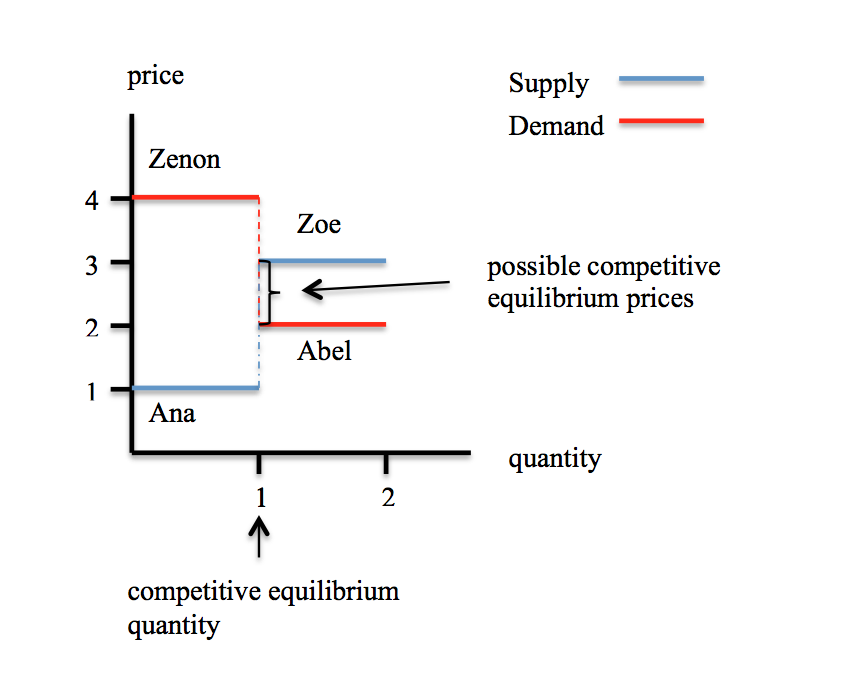

But before we move on, let’s illustrate what we mean by competitive equilibrium and by its efficiency property. We will do it with an example that also helps to illustrate the kind of experiments that have been performed on market mechanisms.

Say Ana can produce a good at the cost of one euro and that Abel values it at two euros. A price between the two valuations (one and two euros) seems a plausible price for the good to be traded. Consider now that Zoe can produce the same good at a cost of 3 euros and that Zenon values the good in 4. Now, a price between 3 and 4 should result in trade for both of them. However, if the four of them meet in a public place, market theory predicts that Ana will trade with Zenon, and that the price will be between 2 and 3 euros, while Abel and Zoe will find no one to trade with. This way, a surplus of 3 euros is generated (if the price is 3, Ana gains 3-1=2 euros and Zenon 4-3=1). Had Ana traded with Abel and Zoe with Zenon, the total surplus in the economy would have only been 2. We say that the first trade is efficient (3 is indeed the maximum possible surplus in this example) and that the second is not.

In the competitive model, markets are shown to have an equilibrium point that sets the price at which products are bought and sold: the place where supply and demand curves meet (see the figure). This static definition was first defended as a result of a simple dynamics: if demand is greater than supply, suppliers will increase the price, if it is lower, they will compete to sell, thus reducing the price. This dynamics is known as the tâtonnement process.

A first attempt to obtain experimental data about competitive equilibrium was conducted by Chamberlin (1948) 1. In his seminal paper, participants in a market experiment could wander about the classroom and negotiate in dispersed groups. These participants are many individuals like Ana, Abel, Zoe and Zenon in our example, and with a wider variety of costs and values. But the experiment found price dispersion rather than converge to the equilibrium point. It was Vernon Smith (1962) 2 who discovered a surprising, rapid convergence to the predicted equilibrium just by adding the feature that negotiated prices could be publicly known. The experiment is technically known as a “double auction posted offer market” (double auction, in short).

Later on, Smith (1982) 3 showed experimentally that the information needed for markets to work was minimal. Agents need to know only their private valuations and the public prices. This constituted the experimental proof of a version of the Hayek conjecture that was theoretically proved by Hurwicz (1960) 4 in a theorem saying that any efficient economic mechanism needs at least n-1 messages, were n is the number of goods. Since individuals in the market need to know only n-1 relative prices (the price of the numéraire good, money, is set to 1), the minimum is achieved. A central planning mechanism, on the other hand, needs to exchange a huge number of messages to work.

Still agents are required to be rational, perhaps one of the most criticized assumptions of the model and at the same time one of the least understood. In the model, rationality means two things, first, that agents have defined, transitive preferences, and, second, that they take actions to satisfy those preferences. Again, this is a sufficient condition for markets to work, and is a condition that has been relaxed. For instance, Becker (1962) 5 was able to show that some features of the model, like the downward-sloping demand functions, can be derived as market-level consequences of random choice behavior subject to budget constraints. The next landmark work in double auction mechanisms came when Gode and Sunder (1993) 6 showed the same result for the equilibrium convergence: if experimental subjects are replaced with computer programs that make random offers subject only to the budget constraint, the result is very close to the competitive equilibrium.

This later result helps to explain the remarkable fact that the double auction market has been shown to work as the theory predicts with all kinds of agents: educated and illiterate, economists and philosophers, house keepers and high level managers.

However, there were still two problems with the model. First, the efficiency level of the random programs was not 100% (the authors reported around 90%), and it was shown to work when there was only one market. Second, even with rational agents, the postulated tâtonnement process for the theoretical equilibrium convergence did not work for all possible competitive markets. Some alternative dynamics have been suggested to replace the original tâtonnement, but the choice seemed to be between a simple dynamics that not always converged to the equilibrium and a complicated one that did.

Crockett, Spear and Sunder (2008) 7 address the issue and find a simple learning rule that converges to the competitive equilibrium. In the new tâtonnement process, rather than changing the price according to whether there is an excess demand or supply, agents change it depending on whether they are subsidizing others at the current prices.

This work must not be understood as the authors claiming that agents actually behave that way. Rather, it just shows that a little learning is sufficient to achieve the competitive equilibrium, and thus opens the door to find other sufficient, mild conditions, and also calls for the gathering of experimental data regarding these learning procedures. Finally, the model is applied to an exchange economy, and it is still waiting to be extended to the production part of the economic activity. The research along these lines continues.

References

- Chamberlin, Edward 1948. An experimental imperfect market. Journal of Political Economy 56, 95-108 ↩

- Smith, Vernon 1962. An experimental study of competitive market behavior. Journal of Political Economy 70, 111-137 ↩

- Smith, Vernon 1982. Markets as economizers of information: Experimental examination of the “Hayek hypothesis”. Economic Inquiry 20, 165-179 ↩

- Hurwicz, Leonid 1960. Optimality and informational efficiency in resourceallocation processes in Mathematical Methods in the Social Sciences, edited by Kenneth J. Arrow, Samuel Karlin, and Patrick Suppes. Stanford: Stanford University Press. Also in Readings in Welfare Economics, edited by K. J. Arrow and T. Scitovsky. New York: Irwin, 1969 ↩

- Becker, Gary 1962. Irrational behavior and economic theory. Journal of Political Economy 70, 1-13 ↩

- Gode, Dhananjay; Sunder, Shyam 1993. Allocative efficiency of markets withzero-intelligence traders: Market as a partial substitute for individual rationality. Journal of Political Economy101, 119-37 ↩

- Sean Crockett; Spear, Stephen; Sunder, Shyam 2008. Learning Competitive Equilibrium. Journal of Mathematical Economics 44, 651–671 ↩

6 comments

The rationality assumption is not well understood, probably because it is somehow counterintuitive. Besides, one tries to find dramatic flaws in the theory when reality diverges significantly from model expectations like in speculative bubbles, and the like.

People illiterate in physics seldom try to criticize string theory (although it is not too strong) because it does not affect their lives. But with economy this is not the case, we are told that certain not desired situations in our life are inevitable consequences of scientific laws of this discipline. Maybe a better differentiation between “scientific economics” and “ideologically driven economics” would be useful for everybody (except for those cheaters trying to convince us that their ideology is science). So articles like this one are especially interesting. However I´ll have to read it again once more (at least) 😉

Dear Joaquín,

Thanks for your comment. If you are told that some non desired situation is inevitable by the laws of economics, consult an economist that speaks with a good knowledge of Economics. Most often, these things are told by politicians or by very biased economists. Some try our best to separate the facts from the ideology. The profession, at least as it is understood by the standards of academic journals, is committed to that.

Ironically, this article seems further evidence of the limited experimental basis for economic theory. But I sincerely hope that this impression is due to my ignorance of the subject. So, is there a review article of the experimental basis of economic theory? What do you think about Steven Keen’s critique in his book Debunking Economics?

I fail to see how experimental evidence if favor can be seen as little experimental evidence. The reported experiments have been repeated one and again, always with the same results.

Steven Keen is the perfect example of the scholar thinking that “everybody is mistaken but me”. He not only thinks mainstream Economics is wrong (Economics in the sense of the study of economic systems), but also that any heterodox school is wrong (or at least, far from being right). You may read him at your own risk, but if you do it without a good knowledge of Economics and with a good ideological bias you will easily be lured by him.

For instance, Keen says that the mathematical model of competitive markets is inconsistent: it asumes infinitely many firms or, alternatively, a price taking behavior. One must say that the first condition does not make the model mathematically inconsistent. It may be unrealistic, but not inconsistent.

The alternative, the price taking behavior, is indeed inconsistent with profit maximization if there are finitely many firms, but is a very good approximation. It largely simplifies the model to make it more tractable. How good an approximation? Theoretically, perfect competition is achieved as the number of firms goes to infinite, and in most models less than 10 firms is enough to see almost no difference. Experimental evidence shows that most times 4 or firms is enough.

Other critics by Keen are no better than this. He may be right in some claims, but his analysis does not provide the proof.

“I fail to see how experimental evidence if favor can be seen as little experimental evidence. The reported experiments have been repeated one and again, always with the same results.”

That’s the reason I asked for a review. They seemed just a few time-scattered references and it not clear if that is all there is or you just point to the ones you thought were the most relevant.

I thought that the phrase saying that “the double auction market has been shown to work as the theory predicts with all kinds of agents” was enough to show that there is plenty of replication. May be it was not. Then I am glad that your comment brought the subject up and thus could be clarified.